A Bumpy Ride

The whiplash continues.

Tuesday’s worse-than-expected inflation data resulted in the worst daily loss for markets since the early days of the pandemic in March 2020.

The NASDAQ fell 5.2%, while the S&P 500 dropped 4.3%.

The August inflation print, widely expected to show falling U.S. inflation, showed the opposite.

Falling gas prices and improving supply side pressures were not enough to offset price increases in both food and shelter.

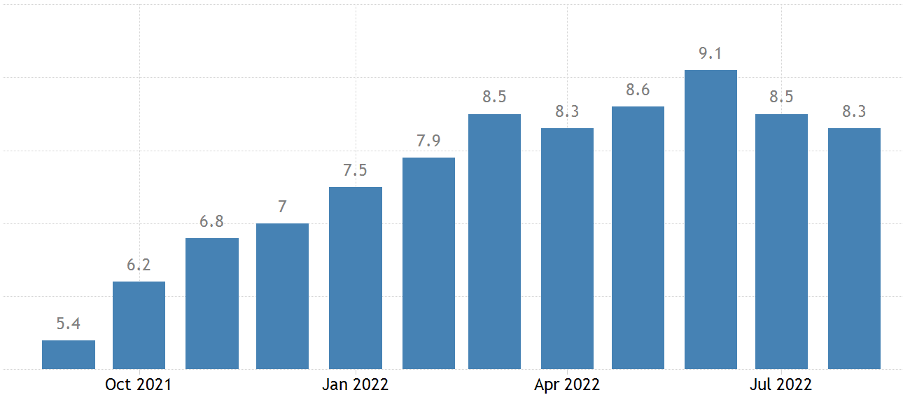

CPI climbed 0.1% month over month in August, accelerating from 0.0% in July.

Year over year inflation numbers fell by less than expected to 8.3%.

Year over Year Change in Consumer Price Index

Source: Trading Economics

Even though we’re talking about just one report, it’s enough to raise doubts about inflation being under control which has knock-on effects regarding how aggressive the Fed needs to be as they attempt to cool the economy.

While this is undoubtedly a negative indicator that was always going to trigger a sell-off in the short term, if we zoom out, I’m not sure it considerably changes the position we are in.

A 75bp interest rate hike is now all but guaranteed at the upcoming Fed meeting this Wednesday.

But I would argue that this was on the horizon regardless.

The Fed were going to stay on track to tighter monetary policy whether inflation was 8.1% (expected) or the 8.3% reported.

As long as inflation rates are anywhere near as high as they are being reported, the Fed will roll out their tighter monetary policy.

This will ultimately suppress demand and cool the economy, increasing market pressure.

Earnings Lead Everything

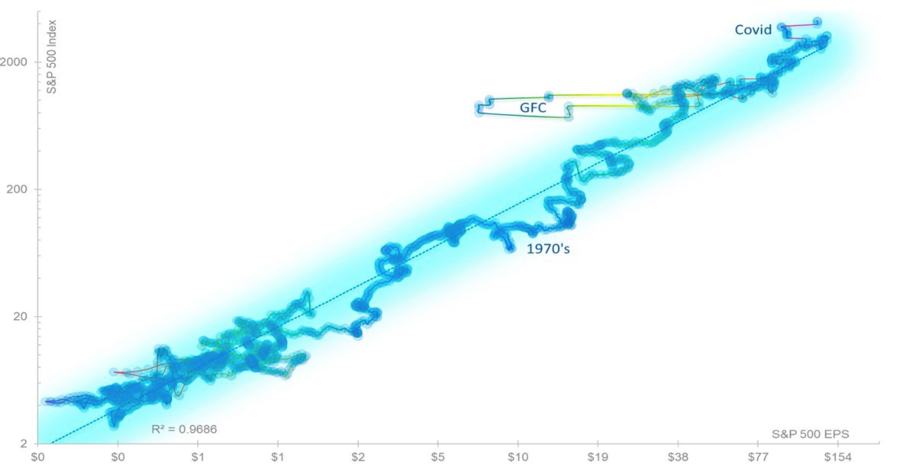

As I have previously discussed, earnings drive the stock market over the long term.

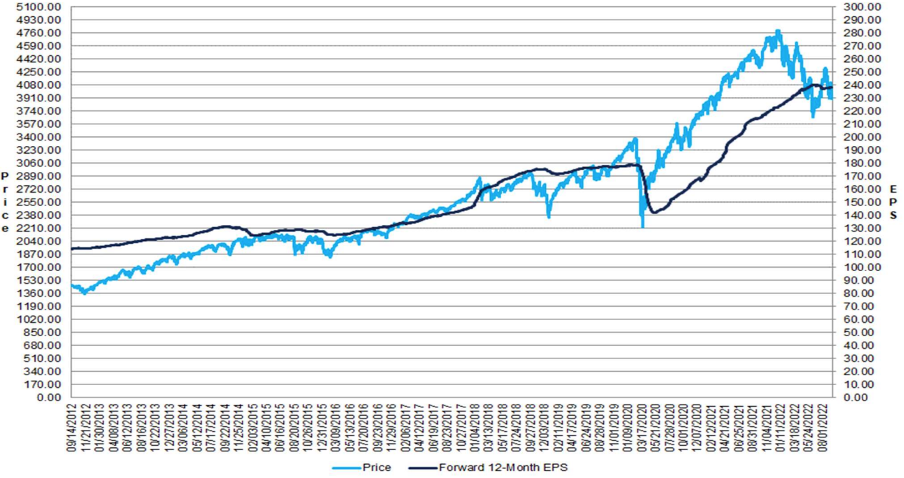

While stock prices are volatile in the short run, a move in a company’s stock price can ultimately be explained by the underlying company’s earnings as shown in the chart below.

Stock Price vs. Earnings

Source: Fidelity

Since 1871, the trend in earnings growth has done a remarkable job of explaining how stock prices behave.

So, while stock prices can be volatile, they move in line with earnings growth over the long run.

This is important to remember as we review the stock market exuberance in 2021.

It’s easy to proclaim that the stock market gains in recent years have been unjustifiable given the seemingly exponential growth we have experienced and, therefore, presume that prices must fall dramatically in order to mean revert.

But it’s vital to remember that higher earnings drove these stock market gains.

The upward trend in earnings supported the higher stock prices we have seen.

While there were obvious corners of froth in the market, Broadly, stock prices rose based on earnings, not blind enthusiasm.

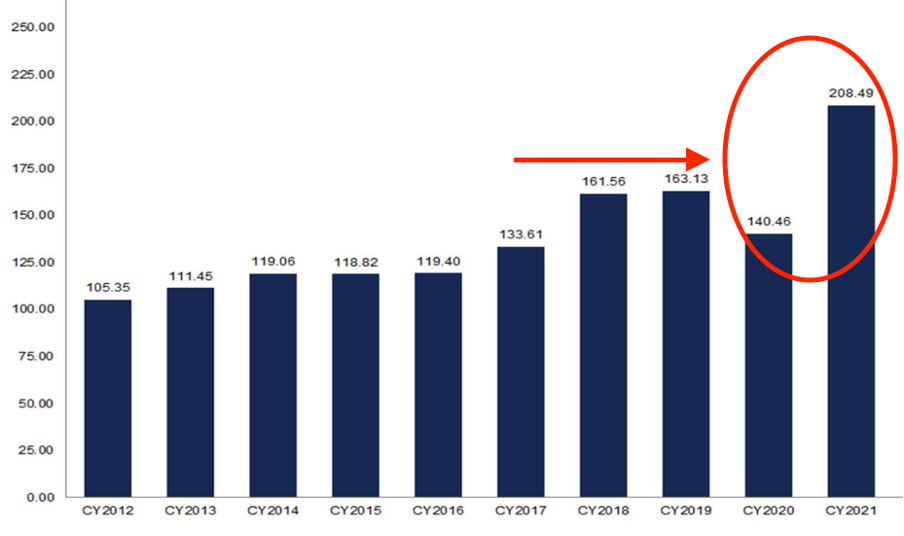

The S&P 500 Saw Huge Earnings Per Share Growth In 2021

Source: Factset

But as fears of an economic downturn intensify, the earnings growth that supported markets in recent quarters is starting to stall.

So what does that mean for stock prices?

Earnings Outlook

One of the most perplexing market trends of 2022 has been the resistance of earnings in the face of higher inflation and rising interest rates. ( top tip: Energy has a lot to do with it)

The Q2 earnings season was better than expected. The S&P 500 earnings growth rate for the second quarter was 6.7%. While this is the lowest earnings growth rate since Q4 2020, this was expected given the difficult comparison to unusually high earnings growth in Q2 2021 and continuing macroeconomic headwinds.

All things considered; this was a win for the stock market.

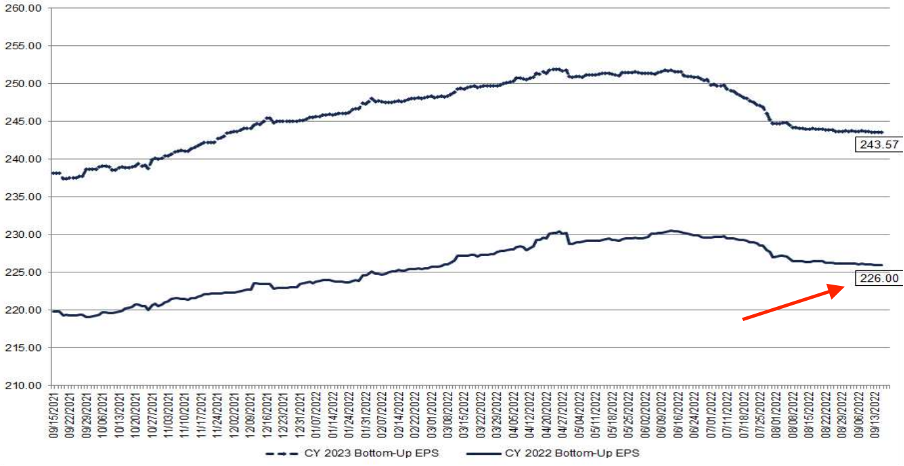

But as we approach Q3 earnings season, we are starting to see earnings estimates slip. The estimated earnings growth rate for the S&P 500 for Q3 is currently 3.5%.

According to FactSet, this is down over 6% from the 9.8% estimated earnings growth rate predicted on June 30th.

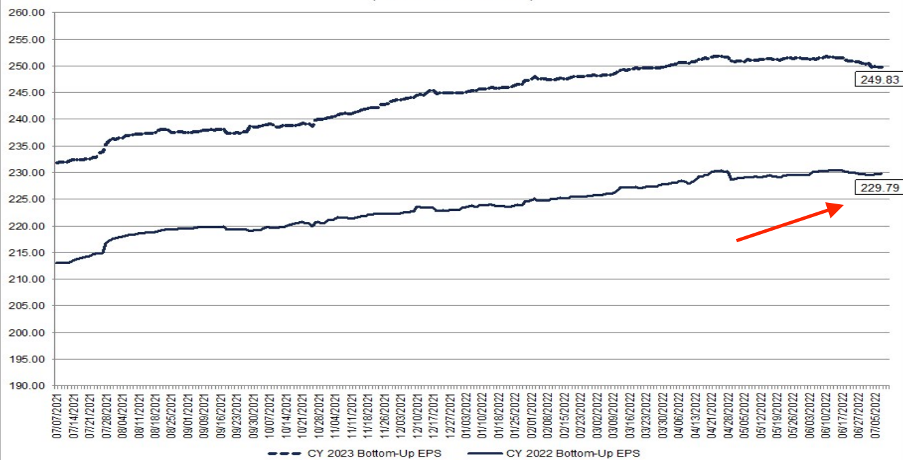

This has reduced the estimated S&P 500 earnings for 2022. 2022 EPS estimates have fallen from 229 per share on June 30th to 226 per share as of August 31st.

S&P 500 EPS Estimates June 30th

Source: Factset

S&P 500 EPS Estimates August 31st

Source: Factset

Of course, these are just estimates but the trend is telling.

Lower company earnings beget lower company stock prices so should investors be running for the hills?

All is Not Lost

Falling earnings growth rates are never what you want to see as an investor, but there are some important factors to consider.

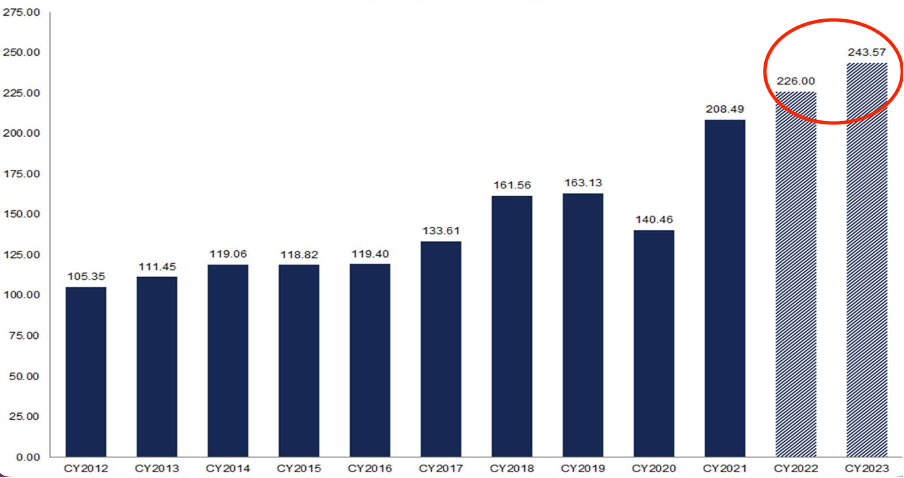

Firstly, slower growth is still growth.

Despite the downward revisions, earnings are still expected to grow 8% in 2022 and another 8% in 2023.

Estimated Growth Rate of 8% in 2022 and 2023

Source: Factset

With projections still positive, revisions would have to fall much more to signal an economic contraction.

Secondly, the market is a forward-looking machine.

The S&P 500 is already down over 19% this year.

Higher inflation and rising interest rates coupled with the relentless growth we saw in 2021 meant that falling growth rates were inevitable for some time, and as a forward-looking machine, much of this has already been priced into the market.

Essentially the market has front run this expected fall in earnings growth.

Valuations have pulled back almost 20% but earnings growth remains positive, which has resulted in a significant improvement in valuation metrics.

The forward 12-month P/E ratio for the S&P 500 is currently 16.4. This P/E ratio is now below the 10-year average of 17.0.

S&P 500 Change in Forward 12-Month EPS vs. Change in Price

Source: Factset

This recent price correction has created a much more intriguing entry point for investors.

Outlook

Volatility will remain.

As long as inflation runs high, Fed policy will continue to negatively affect stock prices and prevent any significant march higher.

In the short term, more pain may lie ahead for both the economy and the stock market, particularly if we see interest rates climb towards or above 5%.

But remember, much of these headwinds have already been priced into the stock market, meaning the stock market will bottom long before the economy does.

The bottom is closer than you think.