My medication is kicking in. I gained 12kg. I had my first beer in about 3 months and the website hit 10k visits in a month. February was good to me..But things weren’t so good for the stock market.

I can’t recall a time in my career when the outlook was so ‘uncertain.’

I write to clarify my thoughts on the market, but right now, the market noise is deafening.

Soft-landing, no-landing, zero-gravity economy, inflation woes, the lag effect of interest rate hikes, monetary tightening, slowing growth, relentless labour markets, falling earnings and more money in the system than ever before….

Pick a few data points and construct whatever narrative you like.

For me, the economic data points to an obvious slowdown, so my head screams ‘LIMITED UPSIDE,’ but my pocket tells me I have been wrong plenty of times before.

The slowing economic data is irrefutable, but using it to discern an exact timeline for the stock market is close to impossible.

And in this game, being early is the same as being wrong.

Ultimately my medium-term view can be condensed to;

With a risk-free rate of 5%, equities offer more downside than upside. Long-lasting bull markets require rapidly expanding valuations and/or strong earnings growth. I don’t see evidence of either in the data.

But this view is contingent on some specific data points.

Here are 3 areas I am watching that will dictate where the market goes over the coming months.

Property

Ultimately housing is the economy. In the U.S., housing makes up 15-20% of annual GDP.

In Ireland, household wealth has soared to 1 Trillion euros. 649 Billion of that was held in property.

You need to pay attention when housing moves a lot in one direction or the other.

Housing data has turned very negative in recent months. Some of the data is shockingly bad.

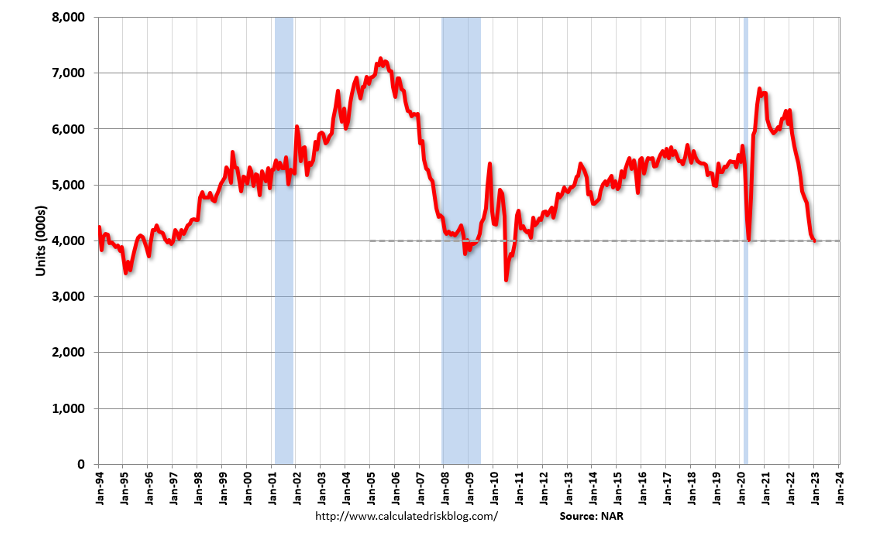

Existing-home sales have been falling for twelve months straight. January year-over-year sales were down 36.9% and are now at levels last seen during the COVID low and Great Financial Crisis.

Existing Home Sales

Source: ,www.calculatedriskblog.com

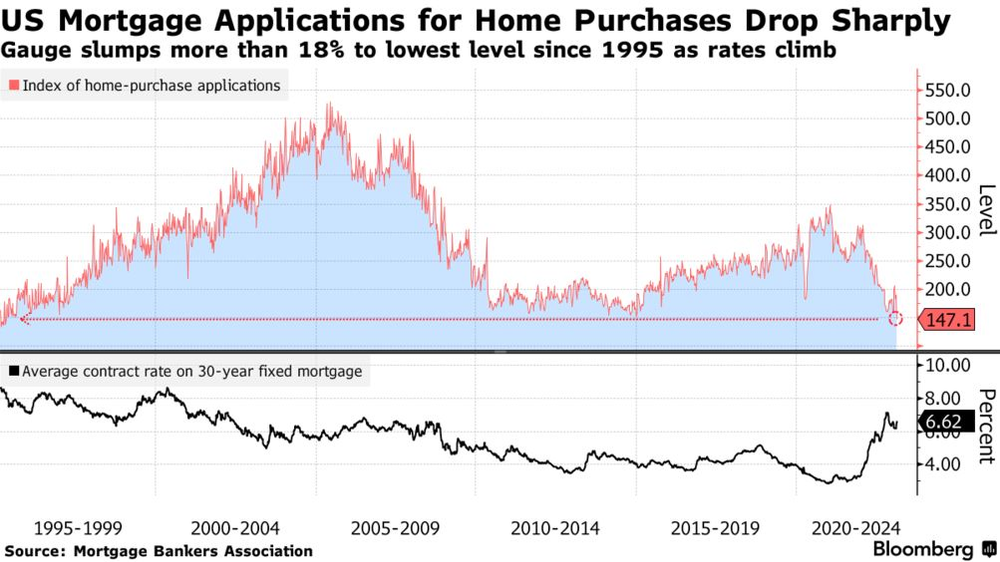

The pipeline isn’t looking much better. Mortgage application rates have hit 28 year lows.

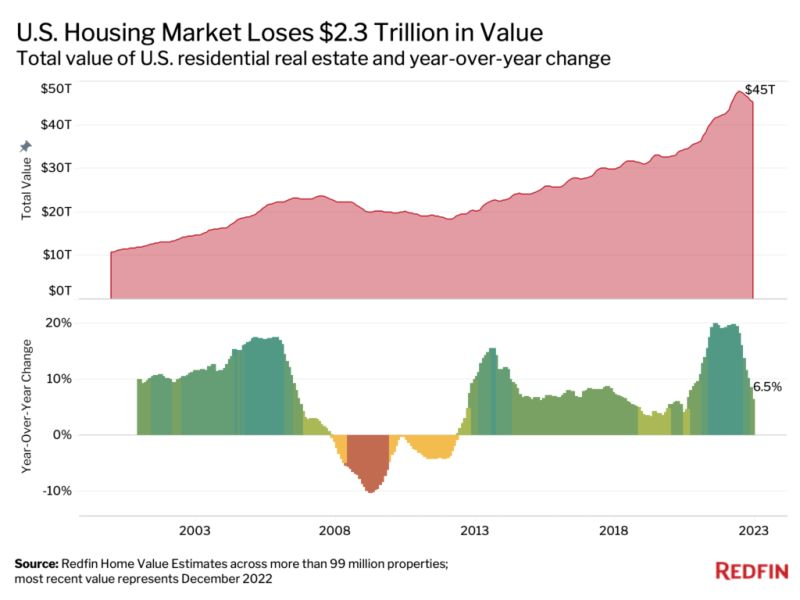

House prices have started to come down, but not by all that much, given that prices soared over 40% in the 18 months from 2020 to June 2022.

Source: Redfin

Signs of Improvement

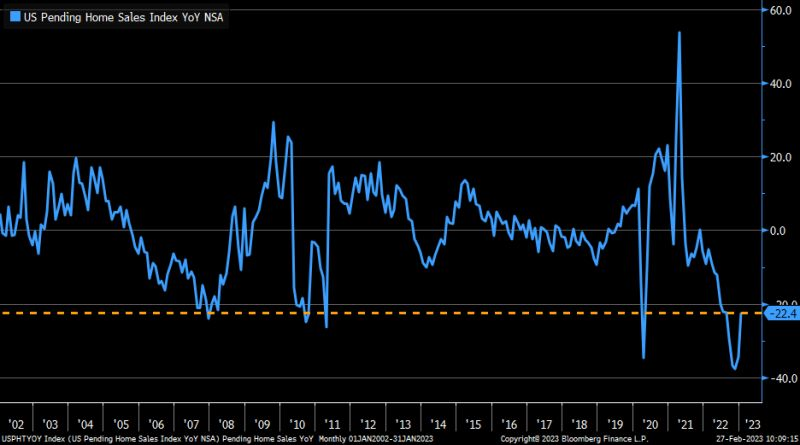

Recently there has been some data suggesting that the market may be bottoming.

A huge monthly gain in pending home sales last month has started to help turn the year-over-year trend around. That said, sales are still down by 22% over the prior year.

US Pending Home Sales

Source: ,@lizannsaunders

The way I see it, the recent favourable data is due to the brief drop in 30-year mortgage rates. As rates climb back to 7%, conditions will tighten once more.

Outlook

Housing affordability is nowhere near where it needs to be for demand to return.

We need either a big adjustment lower in interest rates, a big decline in prices or some combination of the two.

If the Fed are forced to stay ‘higher-for-longer’, Mortgage rates will remain elevated, and prices will be forced to adjust accordingly. A limitation in supply will put a floor on how low prices will go, but there is still further to fall.

Interest Rates

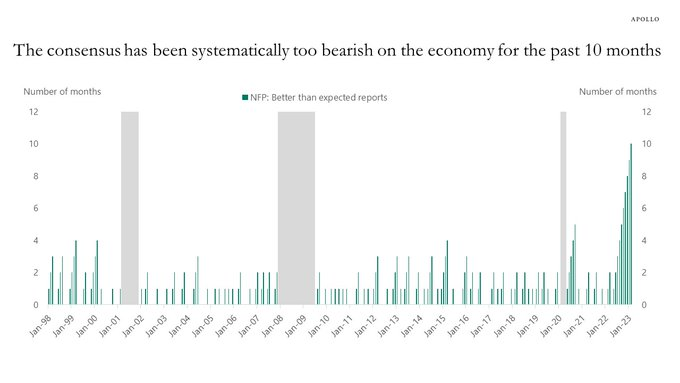

Economic data is surprising on the upside, and markets are busy trying to digest what this means for the Fed.

For the past ten months, the consensus has expected a slowdown in the labour market, but every month the data has come in better than expected.

Source: ,Apollo Academy

One reason for this is corporations are holding more long-term fixed-rate debt. The average maturity of bonds issued by S&P 500 companies is 11 years today. Favourable rates have already been locked in, keeping the overall cost of servicing their debt low and helping companies weather an economic slowdown for now.

However, there are some pitfalls to consider.

-

- Interest rate hikes work on a lag. The impact of these interest rate hikes are not fully known until 18 months to 2 years later. Labour market conditions have yet to be fully impacted by the 2022 rate hiking cycle and could continue to decline long after the Fed stops hiking rates.

-

- The data used to determine labour market participation is questionable. If you look at the ‘full-time’ employment data, the pace of hiring may not be as strong as headline data suggests.

You can view all this in multiple ways, but for me, a resilient labour market will force the Fed to stay higher for longer. These higher interest rates act as a chokehold on the business cycle, ultimately deepening the economic slowdown and increasing the probability of something breaking.

Download My Free Investing Ebook

Savings Rates

The personal savings rate in the U.S dropped to 2.3% as of October, down from 7.3% a year earlier. It’s the lowest since July 2005, when the rate hit a record low of 2.1%.

With that said, there has been signs that the savings rate has stabilised in recent months.

The U.S Personal savings rate climber to 4.7% in January 2023.

Despite this recent stabilisation, the trend reversal is clear.

The story goes something like this:

-

- In 2019, our savings rate was in and around the average rate of 10%

-

- Then, a pandemic came along, forcing us to be locked indoors for a few years while the government sent out cheques and cut interest rates. This pushed savings rates to above 30%

-

- Once the world opened up again, we all ran outside to spend our newfound wealth, resulting in a surge in prices and the highest inflation in 40 years.

-

- We continued to spend regardless of inflation thanks to our pandemic savings, but as our accounts dwindle, inflation becomes a much more precarious beast.

If your bank account is increasing rapidly even after adjusting for inflation, you are more likely to spend and therefore, boost economic activity later on.

If inflation is running wild and the cost of getting a loan is becoming more expensive, your bank account is likely to flatline, and so is your contribution to economic activity.

Extremely low savings rate = slower economy

Unfortunately, you can’t define the entire global consumer using one data point (oh, how I wish it were that simple)

Delinquency rates and Household debt to GPD ratios have climbed slightly higher but still remain at historically low levels, so it’s not all bad.

I will need to see more data before a full call can be made on this one, but the trend is less than convincing.

What does this mean for your portfolio?

-

- With a risk-free rate of 5%. There is absolutely no reason to have idol money sitting in a deposit account. 20X your return by moving into short-duration fixed income.

- Long-duration bonds offer less yield but offer true diversification if and when markets turn and rates fall. Should be considered

- We are likely to see some short-lived market rallies as inflation pressure subsides. These will run out of steam over the medium term. No signs of a long-term bull market just yet.

As always, please reach out to me if you have any questions.

Always happy to help.