I have lived abroad for years, so all the investment strategies I created were typically outside of Irish tax considerations.

But over the last few weeks, I have been putting together several investment strategies for Irish-domiciled clients. It has been eye-opening, to say the least.

I knew some of the more popular investment products in Ireland were questionable, but as you dive into the KID documentation and the PRIIPS info, you start to realise that they are simply daylight robbery.

In short, most of the Irish market appears to be dominated by a handful of life insurance companies that offer ‘wrapped’ multi-asset funds. This means they offer a basket of stocks, bonds, property etc., all within one investment.

Sound great, right? Not quite.

Let’s look at a more popular example

Investment Ideas Straight to Your Email

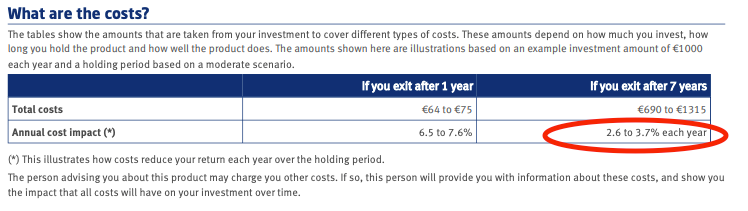

Irish Life’s MAPs 4 multi-asset fund states a standard annual management charge of 1.1%. A bit on the higher side for my liking, but this is still manageable.

But when you dig a little deeper, the KID documents (where all fees have to be fully disclosed as part of UCITS regulations) show the fee as 2.2%.

Double the quoted price.

As an added bonus, they lock your money up for seven years, where an early encashment charge is waiting for those who wish to withdraw their money early. That’s right, they charge YOU for making your money inaccessible.

Bizarre.

For the likes of Standard life, these annual management fees went as high as 3.7%, and that’s not including the early encashment charge.

Standard Life Key Information Document (Synergy Regular Invest)

This lock-up period is a shrewd business tactic. An exit charge is an excellent way to ensure customers don’t leave when they realise how poor the performance is.

Too late, you’re trapped.

Performance

Fees become more digestible provided the performance is strong, but unfortunately, the misery continues.

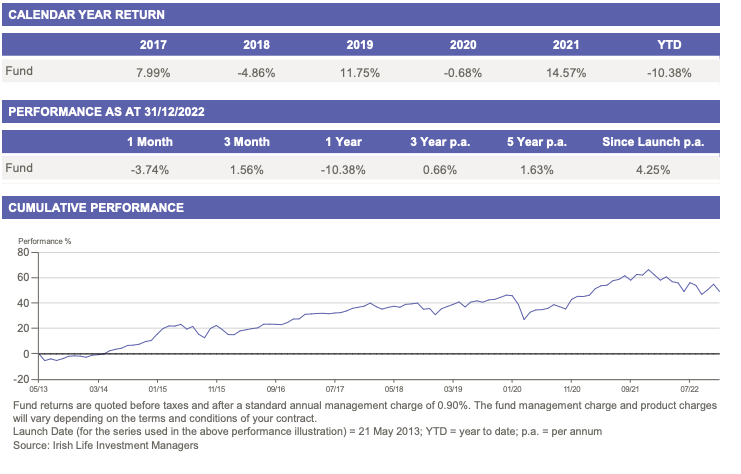

The Irish Life MAPS 4 Portfolio has returned an annual return of 1.63% a year over the last five years. Granted, this was a challenging market climate to navigate, but falling below even the lowest expectations of inflation means that this Fund has returned negative real returns after inflation over the last five years.

Performance and holdings of Irish Life MAPS 4 as of end Decemeber 2022

A similar 60/40 portfolio made up of passive index funds (S&P 500 and U.S T bonds) would have returned roughly 6.5% a year over the same period for a fee of roughly 0.1%. A low custodian fee would also apply here but these charges are negligible in comparison.

We can go round and round in circles regarding the ‘risk adjusted’ approach and the active management blend of the multi-asset Fund versus the 60/40 portfolio I have shown. But the reality is, both products are of comparable risk ratings and composition.

So how can such pathetic offerings still exist in a system where low-cost operators such as De Giro are providing endless ETF options and commission-free trades that provide access to market returns at a much lower price?

Two Reasons Spring to Mind

Firstly, the bulk of the Irish retail investment scene is built on a financial broker commission system where unsuspecting customers are shoved into these products by ‘financial planners’ who receive kickbacks and commissions from these investment companies. You think you’re getting free investment advice? Believe me; you’re not.

No free lunches here.

Second, the tax treatment of ETF structures is comical in Ireland, and US ETFs aren’t even an investment option. A 41% exit tax and an 8-year deemed disposal rule leaves investors stuck between a rock and a hard place.

Choose an overpriced, underperforming product that locks your money away for multiple years or choose the cheaper, better-performing product and suffer the tax consequences.

Bizarrely investors are forced to make investment decisions based on preferential tax treatment rather than on the underlying investment’s merits.

Need to put an investment plan in place?

So what are the exact investment options when you take everything into account?

It can be broken done into 3 main options.

1. Real Estate

The darling of Irish investment options. This has been an entire generation’s de facto’ investment plan’ but this just isn’t an option for so many people today

We are all well-versed in the pros and cons at this stage

Pros

• High potential profits thanks to the leveraged nature of the investment

• Gains taxed at 33% or bit at all if it’s your Principal Private Residence

• Potential for rental income and write off of related expenses over time

• Familiar and tangible

Cons

• Potential for significant losses due to the leveraged nature of the investment

• Active management of any tenants

• Higher mortgage repayments and down payment costs for investment properties

• Potentially high maintenance costs

• Illiquid assets with multiple costs incurred when buying and selling

We could dive deeper here, but I don’t want to get too exhaustive with these lists.

Tax considerations.

Taxed at CGT rate of 33% on all gains

Tax on rental income is at your personal income rate + PRSI + USC. Unless your non-Irish resident, then you will pay a flat rate of 20% income tax.

There are other benefits, such as your ability to write down expenses from a tax perspective or rent-a-room relief, but I am speaking in general terms here.

I will dive more into this and whether or not real estate is a good investment for our generation in tomorrow’s newsletter.

2. Irish and EU domiciled ETF’s/Index Funds

(This includes insurance company equity-based investment products and UCITS funds)

Pros

• Low-cost management fee

• Strong historical performance

• Highly Liquid – you can sell at any time

Cons

• Higher tax on gains relative to real estate and individual stocks

• Dividends taxed at your marginal rate of income tax

• Can’t carry forward capital losses to offset future gains

• Losses made on one ETF can’t be offset against gains made on other ETFs you own.

• Not eligible for annual capital gains allowance of 1,270 euros a year

• Have to pay taxes every eight years whether you sell or not (deemed disposal)

Tax considerations

Exit tax on gains and dividends appears to be 41% (you can avoid recurring dividend taxation by investing in accumulating ETF’s).

ETFs would be the obvious investment option if all else were equal, but in Ireland, all else is not equal.

The deemed disposal rule take the legs from under any wannabe long-term investor looking to maximise the positive effects of compounding over time.

The inability to offset the gains and losses of different ETFs provides a more compelling case for the Multi-Asset offerings that we know and love.

The higher exit tax relative to other investment options will ultimately affect your bottom line when you do look to take profits.

Why the government insists on penalising a more diversified and affordable investment option is beyond me. Fund managers have lobbied for change here, but the government refuses to reduce the exit tax rate in line with DIRT which is now 33% despite DIRT and exit tax being aligned with capital gains tax rates for the last 20 years) .

Now that these tax rates are no longer aligned, investors are forced into poor investment options based solely on preferential tax treatment.

Worth mentioning that US Domiciled ETFs and index Funds (which had a more beneficial tax structure) are no longer available to purchase by Irish retail investors due to EU regulations.

3. Individual Stocks

Pros

• Lower tax on gains relative to Irish/EU ETFs

• Can carry forward capital losses to offset against future gains

• Very liquid – can sell at any time

• Can sell shares with gains of 1,270 euros each year tax-free

• Potential for strong returns

Cons

• Higher risk of loss as all your money is concentrated in just a few companies

• More work involved – If you are doing it yourself, the research involved is endless

• Mental frustration – Trust me, when you are actively making stock picks, the effects of constantly having to make active decisions about your future earnings takes its toll

Tax considerations

Taxed at CGT rate of 33% on all gains

Tax on rental income is at your personal income rate + PRSI + USC.

Tax implications for non-Irish Bonds will be the same, while Irish bonds will have 0% capital gains, not that there would be much gains to report anyway.

From a tax perspective, investing in individual stocks is a better option relative to the ETF and UCIT structures. Still, it is a more concentrated, time-consuming approach that exposes the investor to more risk.

Perhaps an idea would be to not force retail investors into taking more risk as they search for more preferential tax options—just an idea.

You can always reduce the tax exposure of your investments by investing through a PRSA, investment company structures, and other options for those living abroad, but this post is long enough already.

Final word

I’m not some ‘bogglehead’ wannabe trying to cast active investing as the ultimate enemy. I think Fund Managers should be rewarded handsomely if and when they manage to beat the market, so fees are not the enemy here. Charge all the fees you like.

But investing should be a meritocracy. The best investment option wins. In Ireland, there is no level playing field. Instead, you have a minefield. A minefield of non-sensical tax considerations muddying up the water.

As if figuring out what to invest in wasn’t hard enough already.

Feel free to reach out with any questions

Sign up to my newsletter for all my latest market tips and investment advice

If you want me to independently review your investment portfolio, email me at mike@theislandinvestor.com . Always happy to help

Please bear in mind none of this is investment advice and I am not a tax advisor.