Back-to-Back-to-Back

The Fed confirmed their third consecutive 75 bp rate hike on Tuesday in their bid to stomp out inflation.

The rate hike was all but priced in, but the messaging from Jerome Powell drove market sentiment lower.

When speaking about the potential for a soft-landing Powell stated

“the chances are likely to diminish”

When questions on inflation and a potential recession he stated.

“No one knows whether this process will lead to a recession or, if so, how significant that recession would be.”

“I wish there were a painless way to do that. There isn’t.”

Less than inspiring words.

Fed officials also forecast more jumbo-size hikes to come, raising their benchmark rate to roughly 4.4% by year’s end — a full point higher than they had envisioned as recently as June. And they expect to raise the rate again next year, to about 4.6%. That would be the highest level since 2007.

Bear in mind the Fed’s predictions tend to fluctuate dramatically over time.

In June 2021, as the economy showed significant signs of recovery, the Fed were still pricing in 0% rates through the end of 2022 with a 50bp rate hike in 2023.

Instead of sitting at 0% as forecast, the Fed Funds Rate is now at 3.25%.

Not even close.

As inflation and economic data adjust, so too will the Fed’s rate predictions, so try not to take current predictions as gospel.

Market Moves

As a result of the most recent rate hike, stock indexes fell for the fifth time in six weeks to levels near year-to-date lows.

The S&P 500 fell 4.6% and is now down 23.0% from its January 3 closing high and just 0.7% from its June 16 closing low of 3,666.77.

Investors face a big week ahead as the June lows are retested. Friday’s PCE price index release will be crucial. Any signs of lowering inflation will undoubtedly pull markets higher.

Our Obsession with Interest Rates

You may have noticed that many market participants have an unhealthy obsession with interest rates.

But our fear of higher rates is justifiable for the most part.

In short, the Fed has two jobs

-

- Promote maximum employment

-

- Ensure stable prices.

The end.

For better or worse, they only have one tool with which they can do these jobs: Buy and sell securities in the bond markets to loosen or tighten financial conditions.

A.K.A. increasing or decreasing interest rates.

But why are these interest rate adjustments so crucial for the stock market?

As interest rates increase, they place downward pressure on company valuations. Hence the fascination.

Higher interest rates impact valuations in several ways.

From a financial perspective, the future cash flow of a company is discounted by interest rates; therefore, higher interest rates mean a lower present value of future cash flows.

From a relative value perspective, the equity risk premium is reduced. The equity risk premium is the excess returns over the risk-free rate that investors expect to receive given the incremental risks they are taking by investing in the stock market vs. the risk-free rate.

If we consider T-bills as the risk-free rate, then as the yield on T-Bills increases, the hurdle rate equities need to beat to justify the additional risk being taken also increases.

This reduction in the equity risk premium can lead to an outflow from equities into more risk-averse fixed-income products.

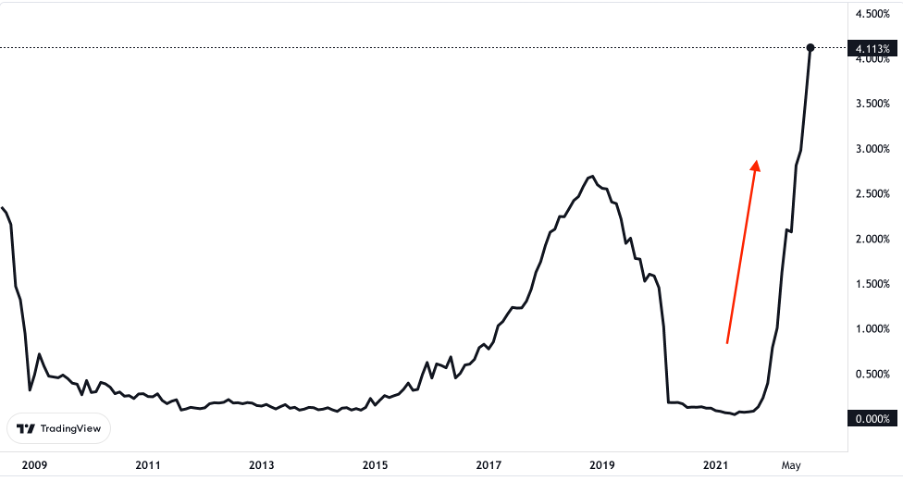

The yield on one-year Treasuries just a year ago was 0.07%, so equities were the obvious choice vs. an asset that offered zero nominal returns, but the 1-Year Treasury Rate has jumped 60x in under a year to 4%. A much more compelling offering.

1-Year Treasury Rate Skyrockets

Source: TradingView

In investing, everything is a relative choice, so as interest rates increase, equities become less compelling vs their risk-free counterpart.

More money flowing into fixed income at the expense of equities is an obvious headwind for equity valuations.

From an economic perspective, higher interest rates will increase the cost of credit.

Higher interest rates make loans more expensive for both businesses and consumers. As a result, everyone ends up forgoing upcoming projects or spending more on interest payments.

This reduces the demand side of the economy by reducing the supply of money in circulation, leading to lower inflation (in theory) and weaker economic activity.

Under these higher interest rate conditions, consumers are encouraged to save more and spend less.

In a world where my earnings are your income, and your income is my earnings, this slowdown in consumer spending will reduce business activity and negatively affect company earnings.

And as future earnings fall, so too do the valuations of the companies reporting them as earnings are what ultimately drive the stock market.

For years, anemic inflation levels meant the Fed could keep interest rates low and focus solely on maximising unemployment. Now, as inflation persists, the Fed is attempting a balancing act as they try to decrease inflation without significantly increasing unemployment.

Only time will tell if they can successfully thread the needle, but if the Fed insist on maintaining this current clip, things will likely get worse before they get better.

Market Outlook

The economic outlook is bleak.

Inflation remains persistent, and as such, interest rates look set to increase further, creating less than favourable economic conditions.

But whether the economic outlook is good or bad is never the question we are trying to answer as investors.

The only question that matters is how much of this negative news is already priced into the market.

On average, the market falls roughly 33% during recessions, but of course, not all recessions are created equal.

With the S&P 500 currently down 23% YTD, it appears that a mild recession has already been priced in.

The possibility of a deep recession is still very much on the table as inflation persists. Still, as data continues to soften, we see encouraging signs that inflation may have peaked.

So, while the current economic environment seems apocalyptic, remember, the stock market and the economy are not the same thing, and as a forward looking machine, the market will bottom long before the economy does.